Banking on Credit Intelligence: How Agentic AI is Transforming Loan Decisioning

Credit underwriting is becoming the decisive battleground for modern banking. As lending volumes expand and regulatory scrutiny tightens, the ability to evaluate risk quickly, consistently, and transparently has moved from operational advantage and today is a strategic necessity.

Banks are now turning to AI credit underwriting to replace fragmented data analysis and static scorecards with real-time decision intelligence.

AI-driven underwriting is rapidly replacing manual credit assessment across banks, NBFCs, and digital lenders.

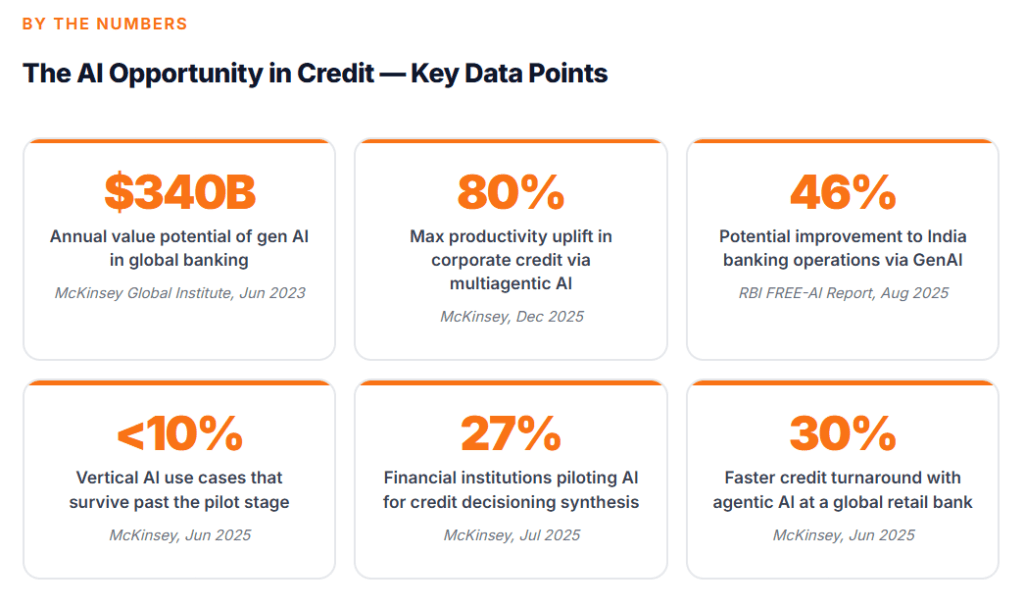

The global explainable AI for credit underwriting market stood at $1.62 billion in 2024 and is projected to reach $12.11 billion by 2033 at a 22.8% CAGR. Closer to home, the Reserve Bank of India's FREE-AI Committee has found that GenAI alone could improve banking operations in India by up to 46%. These numbers point to something larger than an efficiency upgrade credit underwriting is undergoing a structural reinvention.

The question is no longer whether AI belongs in underwriting, rather whether banks have the right kind of Al, one that reasons within policy guardrails.

What is Credit Underwriting? and Why It's More Than Risk Scoring

Credit underwriting is the process by which a lender evaluates whether to extend credit, on what terms, and at what risk. But that description undersells its strategic weight. Underwriting is the institutional codification of a bank's risk appetite.

In banks and NBFCs, underwriting encompasses five interconnected disciplines:

- Financial Statement Analysis Evaluates a borrower's balance sheet, income statement, and leverage ratios against internal benchmarks.

- Cash Flow Evaluation Goes deeper assessing operating cash cycles, debt service coverage, and liquidity buffers rather than relying on stated income alone.

- Sector Benchmarking Contextualises a borrower's financial health against industry peers, recognising that a debt-to-equity ratio of 2x means something very different in real estate versus pharmaceuticals.

- Collateral Assessment Determines the quality, enforceability, and liquidation value of security offered.

- Policy Adherence Ensures that every decision maps to the institution's credit policy, regulatory requirements, and internal risk frameworks.

What is AI Credit Underwriting?

AI credit underwriting uses machine learning, real-time financial data, and policy-driven decision engines to assess borrower risk, automate approvals, and ensure transparent, regulator-ready lending decisions.

✔ improves snippet capture

✔ boosts AI extraction

✔ increases dwell time

The Fault Lines in Traditional Credit Underwriting

Legacy underwriting was built for a different world where loan volumes were lower, data was simpler, and the pace of change was slower. Today's lending environment has exposed its structural weaknesses.

- Manual credit review processes

- Fragmented borrower data environments

- Legacy loan origination systems

- Manual Dependency Creates Inconsistency at Scale

The traditional credit process relies heavily on experienced analysts to review financial statements, interpret ratios, and prepare credit memos.

Credit memo preparation alone can consume over 60 m per application. For NBFCs targeting MSME segments, where ticket sizes are smaller and borrower profiles are diverse, this manual overhead fundamentally limits portfolio growth without proportional headcount increases.

- Data Fragmentation Blinds the Underwriter

A modern borrower's financial health is encoded across multiple systems: banking transactions, GST returns, trade payables, bureau data, account aggregator feeds, and sector databases. Traditional underwriting infrastructure was not built to unify these signals. Analysts end up working with incomplete pictures, triangulating data manually rather than working from a consolidated, real-time view of borrower health.

This is particularly acute in India's DPI-enabled lending ecosystem, where GST data, UPI transaction histories, and Account Aggregator frameworks now offer unprecedented visibility into business cash flows but only to institutions with the integration infrastructure to consume them.

- Static Scorecards Fail Dynamic Sectors

Most traditional credit scorecards were built on historical loan performance data, calibrated during specific economic cycles. They struggle to adapt when sectors experience structural disruption as happened across logistics, retail, and hospitality during the pandemic or when a borrower's profile doesn't fit the historical Mold. The result is either over-cautious rejections of creditworthy borrowers or under-cautious approvals of deteriorating credits.

Sector benchmarking in traditional models is often a manual, periodically updated exercise rather than a continuously refreshed signal. This temporal lag is a material risk in volatile credit environments.

- Traceability Gaps Create Regulatory Exposure

When an RBI examiner or internal auditor asks why a particular loan was approved despite a policy deviation, the answer must come from documented decision logic not from the memory of the analyst who worked the file. In traditional underwriting processes, this reconstruction is often unreliable.

India's RBI has been direct on this point. Its FREE-AI Committee Report (August 2025) explicitly calls for AI models to be transparent, explainable, and fair and flags that erroneous outcomes in AI-powered credit evaluation create legal risk, regulatory sanctions, and reputational harm.

- Scaling Constraints Punish Growth

The arithmetic of traditional underwriting is punishing at scale: more loans require more analysts, more analysts require more supervision, more supervision requires more management overhead. For banks and NBFCs pursuing aggressive SME lending growth, this headcount-to-volume dependency becomes a strategic bottleneck.

It is worth being precise about where generative AI fits into this picture.

LLMs are genuinely useful for drafting credit memos, summarising financial statements, and generating first-pass analyses. But generative AI cannot independently align decisions to structured policy frameworks, execute conditional escalation logic, or maintain a governed audit trail tied to specific credit policy provisions.

Build Smarter Lending with AIA Complete Guide to AI in Credit Underwriting: From Automation to Agentic Intelligence

The AI transformation of underwriting is not a single technology event. It's a progression through three distinct capability tiers automation, augmentation, and agentic intelligence each adding a different kind of value.

Tier 1: Embedded Intelligence Inside Loan Origination Workflows

The foundational layer is AI that lives inside the loan origination process rather than sitting adjacent to it. This means automated policy checks that fire as data is ingested, real-time exception flagging when a borrower metric crosses a threshold, and structured data extraction from documents that populates underwriting models without manual transcription.

When AI is embedded in the workflow catches issues at origination directly than during credit committee review. This compresses cycle times and improves consistency where every application is evaluated against the same policy rules, every time, with no variation for analyst experience or workload.

The McKinsey Global Institute has found that generative AI could deliver $200 to $340 billion in annual value to banking equivalent to 9 to 15 % of operating profits largely through productivity gains in exactly these kinds of knowledge-intensive workflows. But the qualifier is critical if the use cases were fully implemented. Full implementation requires infrastructure that goes far beyond productivity tools.

Tier 2: DPI and Structured Data Integration

India’s DPI ecosystem is emerging as a global model for data-driven lending infrastructure.

GST filing patterns reveal revenue consistency and business seasonality. UPI transaction feeds show payment behaviour, vendor relationships, and cash cycle velocity. Account Aggregator frameworks enable consented data sharing across financial institutions.

The RBI's FREE-AI Committee directly acknowledged this, noting that AI has the potential to expand credit access to the underserved through "alternate credit scoring" and "multilingual chatbots, automated KYC, and agent banking “and that AI can evaluate the creditworthiness of potential borrowers by analysing non-traditional data for those not served by traditional banking systems.

Tier 3: Agentic AI The Reasoning Layer

Agentic AI in lending refers to AI systems that execute policy-based decision logic, trigger credit workflows, and generate explainable outcomes aligned with regulatory frameworks.

Agentic AI represents the most significant evolution in underwriting capability. Where generative AI produces content, agentic AI executes governed logic. In an underwriting context, this distinction is critical.

An agentic underwriting system evaluates borrower context holistically financial ratios, sector positioning, cash flow trends, collateral quality, management track record against a structured policy framework. It executes conditional logic: if leverage exceeds threshold X and sector risk is elevated, escalate to committee review; if cash flow coverage is strong but collateral is thin, apply stress test Y. It triggers escalation protocols automatically, routes complex cases to senior underwriters with pre-populated analysis and simulates stress scenarios against policy-defined risk parameters.

McKinsey's June 2025 research on agentic AI documents this precisely. Relationship managers at a retail bank were spending weeks writing credit-risk memos manually from at least ten different data sources. In the agentic model, AI agents extracted data, drafted memo sections, generated confidence scores, and suggested follow-up questions.

The result: a potential 20–60% increase in productivity, including a 30% improvement in credit turnaround.

For full corporate credit workflows, the gains are even larger. McKinsey's December 2025 analysis of end-to-end credit processes at financial institutions found that multi agentic AI can deliver 40–80% productivity uplift per use case, greater consistency of outputs, and increased automation of control coverage.

Accelerate Loan Approvals with AIHow AI Transforms the Credit-Risk Memo Process

Traditional credit memo preparation requires analysts to manually gather borrower data, validate documents, perform financial analysis, and prepare credit notes. This often takes 2–4 days per application.

Agentic AI streamlines this workflow by automatically

- collecting data

- running analytical checks

- generating structured credit insights

Human involvement shifts primarily to final validation and approval.

Continuous Underwriting: The Post-Disbursement Intelligence Layer

Traditional underwriting ends at disbursement. AI-native underwriting does not.

Continuous underwriting uses the same data integration infrastructure that enables better origination decisions to monitor portfolio health in real time.

- Real-time credit risk monitoring

- Portfolio risk intelligence

- Early warning credit systems

Banking transaction patterns, GST filing regularity, and payment behaviour signals are analysed continuously against early warning thresholds.

McKinsey's July 2025 survey of financial institutions found that 27% are now piloting gen AI specifically for synthesizing information in credit decisioning, with early-warning systems and portfolio monitoring among the top use cases. This shift from episodic review to continuous portfolio intelligence is arguably the most commercially significant capability AI brings to underwriting.

Why Banks Need AI-Native Infrastructure, Not AI Add-Ons

This is the distinction that matters most for institutions making technology investment decisions right now. The difference between an AI-native underwriting platform and a bolt-on AI tool is a matter of architecture.

Professional Support and Compliance Ease for MSMEs

Budget 2026 supports ICAI, ICSI, and ICMAI to create short-term courses and a cadre of “Corporate Mitras” in Tier II and III towns, helping MSMEs manage compliance at lower cost. For lean MSMEs, reduced compliance friction directly improves execution focus and working capital discipline.

The Real Cost of Bolt-On AI

Bolt-on AI tools are typically deployed as a layer on top of existing loan origination systems. They ingest data from legacy platforms, generate outputs summaries, scores, flags and pass those outputs back to human reviewers. This creates structural problems.

The first is disconnected data layers. When AI operates on data already processed and formatted by legacy systems, it works with a filtered, often incomplete view of the borrower. The enriched signals from DPI integrations, real-time transaction feeds, and alternative data sources may never reach the AI layer.

The second is weak explainability. Bolt-on tools frequently operate as black boxes relative to the credit policy framework. They may produce a score or recommendation.

The third is compliance risk. McKinsey has explicitly cautioned that "just adding new AI technology on top of existing processes will not lead to transformational change; rather it could lead to a spaghetti of technical debt". And the same McKinsey research that identified the $200–340 billion opportunity in banking also found that fewer than 10% of vertical AI use cases make it out of the pilot phase primarily because institutions are building on top of existing processes rather than redesigning workflows with AI at the core.

The Regulatory Dimension Is Now Non-Negotiable

Two regulatory frameworks are converging to make explainability and audit infrastructure a hard compliance requirement not a best practice.

In the EU: The EU AI Act explicitly classifies AI systems used to evaluate creditworthiness or establish credit scores as high-risk AI systems under Annex III. Full obligations including data governance, transparency, human oversight, conformity assessment, and EU database registration become enforceable on 2 August 2026. Non-compliance carries penalties of up to €35 million or 7% of global annual revenue.

In India: The RBI's FREE-AI Committee has recommended that boards approve AI policies, set up governance structures, and establish standing committees to monitor new AI risks from biased lending models to deepfake fraud to systemic weakness arising from multiple institutions using the same algorithms.

What AI-Native Architecture Looks Like

An AI-native loan origination system has the policy engine embedded at its core.

This architecture includes a structured reasoning layer that applies policy rules to data inputs, executes conditional logic, and generates decision outputs directly traceable to policy provisions and data sources. It includes audit logs built into the workflow so that every data input, policy check, exception flag, and human override is captured as it occurs.

Agentic AI vs. Generative AI: The Operational Distinction

| Capability | Generative AI | Agentic AI |

| Credit memo drafting | ✓ | ✓ |

| Policy rule execution | ✗ | ✓ |

| Conditional escalation logic | ✗ | ✓ |

| Audit trail generation | ✗ | ✓ |

| Stress scenario simulation | Limited | ✓ |

| Regulator-ready explainability | ✗ | ✓ |

| Continuous portfolio monitoring | ✗ | ✓ |

The Next Era of Credit Decisioning

The evolution of credit underwriting follows a clear trajectory. Manual underwriting gave institutions control but not scalability. The next phase AI-native, agentic, policy-embedded underwriting gives institutions all three: scale, adaptability, and the governance infrastructure to operate with regulatory confidence.

Underwriters don't disappear in this model. They move up the value chain.

Power Your OriginationCredAble's AI-powered Low-Code Loan Origination System is built on exactly this principle. The platform embeds credit policy directly into the decisioning workflow, integrates with India's DPI infrastructure for real-time data ingestion, and deploys agentic AI that executes structured reasoning not just content generation. Every decision is traceable, every exception is documented, and every output is aligned to the institution's defined risk appetite.

Get Started TodayFrequently Asked Questions

AI credit underwriting is the use of machine learning, structured reasoning, and real-time data integration to evaluate borrower creditworthiness, execute policy-aligned credit decisions, and maintain auditable decision logic—replacing or augmenting manual credit analysis in banks and NBFCs.

AI improves SME credit access by evaluating:

- Cash flow behaviour

- GST filings

- Banking transaction histories

- Alternative financial data

This enables lenders to assess borrowers who may have limited traditional credit history.

Yes. Modern AI underwriting systems incorporate:

- Explainability frameworks

- Audit trails

- Policy traceability mechanisms

These features align with regulatory expectations, including requirements from the RBI and the EU AI Act.

Generative AI produces content such as drafts, summaries, and analyses.

Agentic AI executes governed logic by:

- Applying credit policy rules to structured data

- Triggering escalation protocols

- Simulating stress scenarios

- Generating explainable and auditable decision outputs

In underwriting, agentic AI functions as the decisioning engine, while generative AI acts as the content layer.

Modern AI underwriting platforms integrate multiple data sources, including:

- GST data

- Banking transaction feeds

- Account Aggregator data

- Bureau scores

- UPI payment histories

- Digital identity verification

- Trade data

- Sector benchmarks

This creates a multi-dimensional borrower profile beyond traditional financial statement analysis.

Credit-scoring AI is classified as high-risk under global regulatory frameworks such as the EU AI Act (Regulation 2024/1689), with full enforcement beginning 2 August 2026.

Regulators including the RBI emphasize that AI-driven credit decisions must be:

- Transparent

- Fair

- Traceable

Unexplainable AI decisions may expose institutions to regulatory penalties, legal risk, and reputational damage.

Continuous underwriting uses real-time data signals—such as transaction patterns, GST filings, and payment behaviour—to monitor borrower health after disbursement.

- Tracks covenant compliance

- Generates early warning alerts

- Identifies credit stress before default events

It transforms underwriting from a one-time approval process into an ongoing portfolio intelligence function.

Industry research indicates significant productivity improvements:

- 20–60% increase in productivity in credit memo preparation

- 30% faster credit turnaround times

- 40–80% productivity uplift across corporate credit workflows (multi-agent AI use cases)

AI augments rather than replaces credit analysts. It automates:

- Data analysis

- Policy checks

- Structured evaluation workflows

Human experts continue to focus on complex judgment, exception handling, and strategic risk management.

Think Working Capital… Think CredAble!