Rising Working Capital Crisis for Defence Startups: Is the Middle East Conflict Breaking or Fueling Defence Supply Chains?

In less than a week, over $11 billion was deployed into active military operations, with munitions expenditure alone crossing $5 billion in the early phase of escalation. The United States’ defence budget has surged to nearly $1.5 trillion, up sharply from $874 billion last year, reflecting the scale at which military preparedness is being funded.

Hours after the ceasefire between US and Iran was announced, several airstrikes have been reported in the Middle East, with new tariff threats of up to 50% on countries supplying defence equipment to Iran. This has introduced another layer of geopolitical and trade uncertainty.

For defence manufacturers, the question is becoming harder to answer.

Does this environment signal a “golden age” of growth, or a more complex phase where execution continues to face increasing pressure.

With billions lost in high-value systems, the immediate challenge shifts to funding the next cycle of manufacturing.

More than 13,000 targets were struck over a 38-day period before a ceasefire was declared with destruction cost scaling over $3–5 billion as of early April 2026, and it is now likely exceeded given continued losses through April.

The Pentagon is expected to account for these losses in a proposed $200 billion supplemental spending request sent to the white house.

The moment assets are lost at this scale; the pressure shifts to re-manufacturing, and that only scales when working capital flows and supply chains hold.

At a macro level, global defence demand continues to expand. Defence spending has crossed $2.6 trillion, while global working capital locked in backlogs are estimated over $700 billion up by 25% in just 2 years.

The challenge now lies in sustaining production through increasingly volatile operating conditions, where supply chains, logistics, and cash flows are subject to rapid shifts within short timeframes.

Production systems are required to move at speed, with inventory, materials, and manufacturing capacity already positioned ahead of demand. The ability to sustain this pace depends on how efficiently capital flows through the supply chain.

This is where the role of working capital becomes central.

Why Defence Contracts Create Working Capital Stress

Defence manufacturing is exposing a deeper constraint across supply chains where capital, capacity, and execution must scale simultaneously.

Defence giants like RTX, Boeing, and Lockheed Martin operate at immense scale, with long production cycles and high-value output supported by deeply interconnected supply chains. This concentration of capital and long production timelines means liquidity gets locked deep in the supply chain, making structured working capital solutions critical to keep suppliers solvent and production uninterrupted.

Defence manufacturing operates on a fundamentally different financial rhythm, defined by long production cycles. Contracts typically run 6 –10 years or more, capacity buildouts take 1 –3 years before output begins, and cash flows are tied to milestone-based payments released at specific stages of project completion.

Payments are released at predefined stages of completion, research on the defence sector identifies this directly: high expansion costs, constrained supply chains, and lengthy order backlogs stretch working capital to breaking point even on fully funded contracts.

Defence manufacturers are struggling to scale output, weighed down by capital-intensive expansion, fragile supply chains, stringent regulatory compliance, and order backlogs that can stretch as long as 7 years for certain OEMs.

Capital is committed long before revenue appears.

J.P. Morgan's Defence supply chain analysis shows inventory rising across the value chain during production ramp-ups, intensifying balance sheet pressure upstream at every tier.Historically, Defence contractors have been absorbing working capital during major scale-ups before cash flows normalise. When defence companies ramp up production, they need to put in their own money upfront before they start getting paid. This upfront money tied in inventory, materials, labour, and production is called working capital absorption.

That absorption is compounding across the entire supply base at once.

Build Capital ResilienceThe Defence Supply Chain Financing Gap

When a geopolitical chokepoint disrupts energy, freight, insurance, and shipment certainty at the same time, the real bottleneck becomes working capital. Defence programmes slow down because cash gets locked before delivery gets completed.

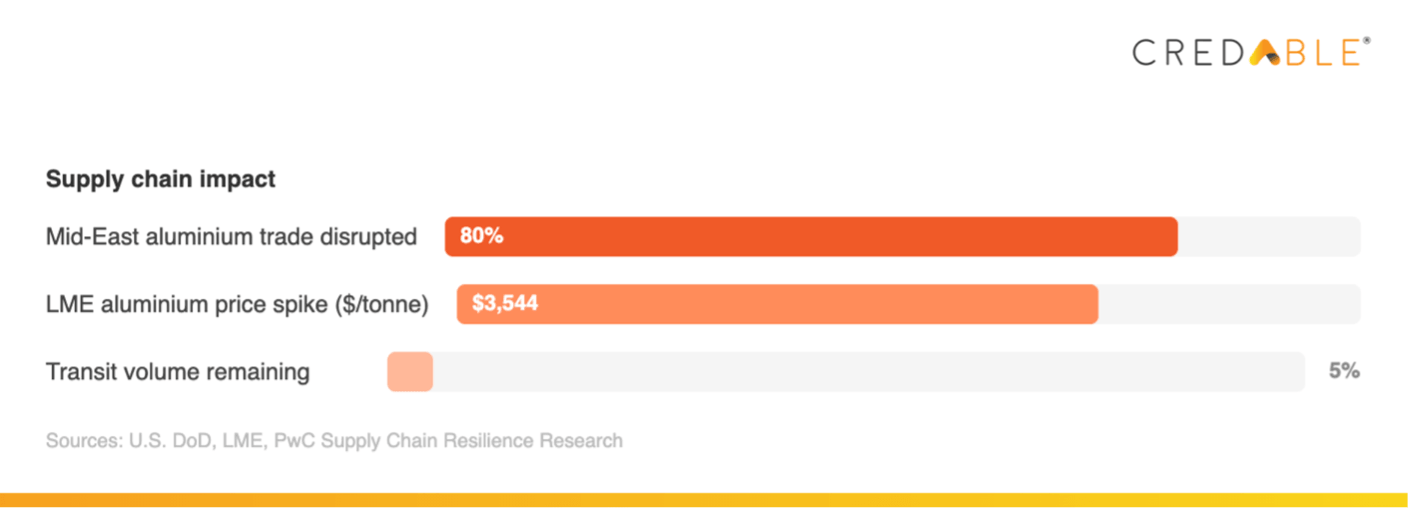

Overall Ship transits dropped about 95% from around 130 per day in February to just 6 in March. Defence raw material transited the same route, out of which aluminium trade from Middle East is 80% and aluminium being a critical material in aircraft frames, missile casings, and armoured vehicle structures transits the same route now is effectively closed. LME aluminium prices spiked to $3,544 per ton as a result. PwC's supply chain resilience research confirms these supply chains were already under geopolitical pressure before the Hormuz closure.

J.P. Morgan's structured Defence financing research identifies the components of fit-for-purpose working capital in defence: inventory finance that stages capital against production milestones, receivables financing that converts government dues into deployable liquidity, and supply chain finance that reaches beyond Tier 1 to fund the full vendor base.

Tier 1 suppliers increasingly participate in anchor-led supply chain finance programmes. Researches have confirmed that structured receivables finance and supply chain finance have unlocked meaningful liquidity at the OEM and Tier 1 level.

Tier 2 and Tier 3 are different. Defence supply chain assessment confirms that financial access deteriorates sharply below Tier 1. These are predominantly MSMEs and Startups which are holding precision machining capacity, certified electronics manufacturing, and specialty materials processing that cannot be quickly substituted.

As production volumes increase, liquidity at these tiers becomes a critical factor in maintaining continuity.

Explore Achor-led Supply Chain FinancingWhy India's MSME Defence exports jump 63% to record ₹38,424 crore

India’s defence production has scaled insanely crossing $16 Bn in 2025 with over 16000 MSMEs emerging as the gamechangers, strengthening indigenous defence capabilities. 788 industrial licenses have been issued to 462 companies. This has effectively led to defence exports rising sharply to a record ₹38,424 crore ($4 Bn) in FY26, registering a 62.66 % increase from ₹23,622 crore in FY25, according to the Ministry of Defence.

The country now exports defence equipment to over 80 nations, with the number of exporters increasing to 145 in FY26 from 128 a year earlier.

The two top favourites from India in the arms market are the BrahMos, which is one of the fastest supersonic cruise missiles, while Pinaka, seen as a cost-effective, high-precision artillery rocket system at competitive prices. Other being Akash-1S Surface-to-Air Missile systems, Pinaka Multi-Barrel Rocket Launchers and Swathi weapon-locating radars and ATAGS howitzers.

This momentum is also reflecting in market sentiment. Stocks such as MTAR Technologies, Astra Microwave Products, and Mazagon Dock Shipbuilders recorded gains of 1–3%.

Brokerages continue to maintain a positive outlook, citing sustained policy support and procurement reforms as key enablers for domestic manufacturers to scale both in India and global export markets.

India's target requires 75% of defence capital procurement from domestic industry. HAL, BEL, L&T Defence, and Tata Advanced Systems are scaling to meet contracted demand.

Supplier ecosystems are now MSMEs and startup-led which are entering defence manufacturing via iDEX and corridors. Execution success hinges on whether these suppliers stay financially solvent through long ramp-up cycles.

Yet beneath this strong demand environment, the nature of execution is changing in a more fundamental way.

Deloitte's 2024 Working Capital Roundup reinforces the outcome: companies that actively managed working capital through major production scale-ups maintained programme performance. Those that did not absorbed cost overruns that outlasted the cycle.

Financing anchored to contract certainty and sovereign counterparty quality rather than solely to historical balance sheet reflects the actual risk profile of a defence supplier. Citi's analysis of traditional trade finance instruments including receivables finance and performance standby letters of credit shows that these instruments exist, but their reach across domestic MSME and Startup supply chains remains limited.

Today we also see The Indian government exploring extending the Trade Receivables Discounting System (TReDS) platform to defence procurement to address long payment cycles for MSMEs. By enabling invoice discounting, this initiative aims to improve liquidity, support capital-intensive production, and enhance participation within defence supply chains.

Unlock Working Capital NowWorking Capital as the Defining Constraint for Driving Defence Execution.

Governments have committed the budgets. Contracts have been signed. Industrial capacity is being built.

The variable that determines whether those commitments translate into delivered programmes is financial infrastructure specifically, whether working capital reaches suppliers at the tier where continuity actually breaks.

Defence has entered a phase of sustained growth.

What determines outcomes now is not demand, but the ability to finance execution across the supply chain.

This is where working capital platforms have a structural role. As infrastructure providing multiple solutions that reaches the suppliers conventional credit does not.

Working capital in defence is a delivery programme consideration. And programme delivery is a national readiness consideration.

Think Working Capital… Think CredAble!