What is a Loan Origination System? A Complete Guide for Banks, NBFCs & Financial Institutions

The loan origination system market, a core layer within digital lending platforms, stood at $10.91 billion in 2024 and is projected to reach $114 billion by 2034, reflecting how lending infrastructure is being rebuilt around speed, data, and embedded decisioning.

Modernising the loan origination system is now tied directly to resilience. It determines how quickly capital can move, how accurately risk can be priced, and how confidently institutions can grow. In a market where liquidity, risk, and execution are tightly linked, the LOS is no longer a supporting system. It is the control layer for how banks operate and compete.

That shift is already visible inside banks, where the loan origination system is becoming the control layer for how credit is evaluated, approved, and scaled. Understand how this transformation is reshaping credit decisioning, risk control, and growth for modern banks.

What is a Loan Origination System?

A Loan Origination System (LOS) also called loan origination software is a technology platform that enables banks, NBFCs, and financial institutions to manage the complete loan lifecycle. It covers everything from product configuration and borrower application intake, through underwriting, approval, and legal documentation, all the way to fund disbursement.

Before loan origination systems became standard, institutions relied on paper-based processes, disconnected spreadsheets, and manual legal form templates to generate loan documents. These approaches were slow, error-prone, and difficult to scale, especially at high loan volumes across retail, SME, or working capital portfolios.

Today, a modern LOS goes far beyond document generation. It orchestrates real-time data collection from credit bureaus and government databases, applies AI-driven credit scoring models, enforces regulatory compliance checkpoints, and triggers automated borrower communications, all within a configurable, scalable platform.

How Does a Loan Origination System Work?

A loan origination system works by integrating all functions involved in lending into a single, rules-driven platform. Instead of relying on loan officers to manually collect data, cross-verify documents, and enter information across multiple systems, the LOS automates and orchestrates every handoff between teams and data sources.

At its core, the LOS acts as a central hub that connects borrowers, relationship managers, credit analysts, compliance officers, and external systems including credit bureaus, KYC APIs, and government databases within a defined workflow. Each stage is governed by pre-configured rules, approval hierarchies, and compliance checks, enabling faster decisions without sacrificing risk discipline.

Modern LOS platforms are built on an API-first architecture, enabling seamless integration with core banking systems, CRM platforms, Digital Public Infrastructure such as India's Aadhaar and GST networks, and third-party data providers. This makes them both interoperable and scalable as lending volumes grow.

What is the Loan Origination Process in Banking?

The loan origination process in Banks refers to the step-by-step journey of evaluating and approving a loan.

The 6 Stages of the Loan Origination Process

Understanding the loan origination process is key to understanding the value an LOS delivers. Here are the six core stages every modern LOS manages:

- Loan Application & Intake The process begins when a borrower submits an application through a web portal, mobile app, branch visit, or via a relationship manager. A well-built LOS supports multi-channel origination: digital self-service for tech-savvy borrowers, and assisted or phygital journeys for those who prefer face-to-face interaction. Submitted data is validated in real time to ensure completeness before moving forward.

- KYC, Document Collection & Verification Once an application is submitted, the LOS triggers automated requests for identity documents (PAN, Aadhaar), address proof, income statements, and bank records. Advanced platforms use OCR and NLP to extract and validate information from uploaded documents instantly flagging discrepancies before they slow down credit review. Digital KYC (eKYC) integrations verify borrower identity within seconds, eliminating routine branch visits.

- Credit Assessment & Scoring Here the LOS evaluates the borrower's creditworthiness. It automatically pulls credit bureau scores (CIBIL, Equifax, CRIF), retrieves GST and banking data, and applies the institution's proprietary scoring models. AI-powered systems go further using alternative data signals, cash flow patterns, and behavioural analytics to assess borrowers who lack traditional credit history. This is particularly valuable for MSME and first-time lending.

- Underwriting Underwriting is the risk decision at the heart of loan origination. The LOS applies parameterised rules, policy guardrails, and credit models to determine whether a loan should be approved, the sanctioned amount, and the rate and tenure. Modern systems support both straight-through processing (zero-touch auto-approval for low-risk profiles) and maker-checker workflows for cases requiring human review. AI-assisted underwriting cuts credit decision time by up to 70%.

- Approval, Sanction & Communication Once underwriting is complete, the LOS generates a sanction decision and automatically notifies the borrower via email, SMS, or in-app messaging. For approved loans, it triggers the generation of the loan agreement, sanction letter, and other required documentation pre-filled with verified borrower and loan data. eSign capabilities allow borrowers to complete signing digitally, removing the need for physical branch visits.

- Loan Disbursement The final stage is disbursement transferring sanctioned funds to the borrower's account. The LOS integrates with core banking and payment infrastructure to trigger disbursement automatically upon completion of all pre-conditions. End-to-end audit trails ensure complete traceability, enabling post-disbursement compliance reporting and exception management.

Key Features of Loan Origination Software

A modern LOS platform for banks and NBFCs includes:

1. End-to-End Loan Processing Automation

Handles the entire lending lifecycle in a single system.

2. AI-Powered Credit Underwriting

Uses data models to analyse borrower behaviour, cash flow, and risk patterns.

3. Integration with Credit Bureaus and APIs

Integration with internal systems and external data sources, which help lenders access verified borrower information faster and reduce the need for repetitive manual data entry.

Connects with:

- Credit bureaus

- GST and tax systems

- Account Aggregator frameworks

- Banking systems

4. Digital Document Management

Document collection and verification are often major bottlenecks in loan processing. A digital Loan Origination System helps institutions manage documents in a more organised, secure, and traceable manner.

Automates:

- Document uploads

- Verification workflows

- eSignatures

5. Compliance and Audit Trails

Every lending decision must be traceable, especially when applications involve policy deviations, exceptions, or multi-level approvals.

6. Multi-Channel Loan Origination

Borrowers today apply for loans through multiple channels using LOS without creating fragmented processes.

It supports:

- Branch-based lending

- Digital lending platforms

- Agent-assisted journeys

Benefits of a Loan Origination System

1. Faster Loan Approval

Automation reduces turnaround time significantly and improves conversion rates.

2. Improved Credit Risk Management

Standardised decisioning ensures consistent risk evaluation across portfolios.

3. Better Customer Experience

Borrowers benefit from:

- Faster approvals

- Real-time tracking

- Simplified digital journeys

4. Higher Operational Efficiency

Manual tasks are reduced, improving team productivity.

5. Scalable Lending Operations

Institutions can handle higher loan volumes without increasing operational complexity.

Types of Loan Origination Systems

1. Retail Loan Origination Systems

Used for personal loans, home loans, and consumer credit.

2. SME and Business Lending LOS

Designed for:

- Cash flow-based lending

- Working capital financing

- Invoice and supply chain finance

3. Corporate Loan Origination Systems

Supports complex deal structures, multi-party approvals, and large-ticket lending.

4. Cloud-Based Loan Origination Software

Delivered as SaaS, enabling faster deployment and scalability.

Loan Origination System vs Loan Management System (LMS)

| Feature | Loan Origination System (LOS) | Loan Management System (LMS) |

| Purpose | Handles loan creation and approval | Manages loans after disbursement |

| Focus | Application to disbursement | Repayment and servicing |

| Users | Credit teams, underwriters | Operations and servicing teams |

Both systems are essential for a complete lending infrastructure.

Challenges Without a Loan Origination System

Financial institutions without a modern LOS face:

- Longer loan processing times

- Manual errors in documentation

- Inconsistent credit decisions

- Limited scalability

- Poor customer experience

These challenges directly impact growth and profitability.

How AI is Transforming Loan Origination Systems

Modern lending is increasingly data-driven.

AI-enabled LOS platforms can:

- Analyse structured and unstructured financial data

- Identify risk patterns in real time

- Generate automated credit summaries

- Improve underwriting accuracy

Industry data shows that AI can significantly enhance banking efficiency and decision-making outcomes.

Capabilities of AI in LOS

- Automated credit memo generation

- Real-time fraud detection

- Cash flow-based lending models

- Continuous borrower monitoring

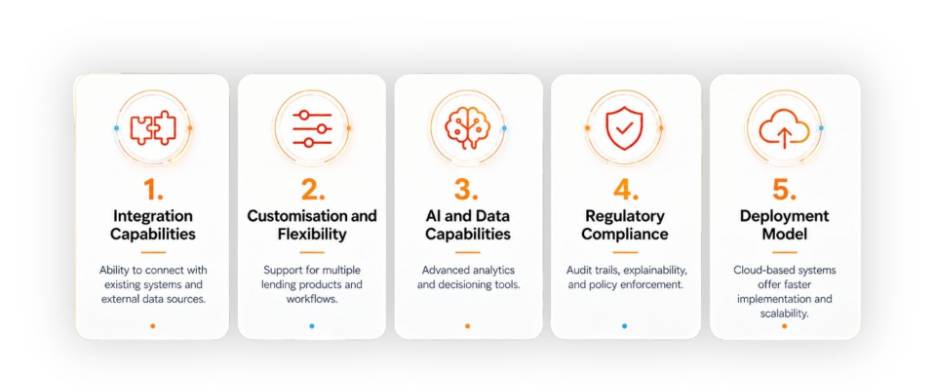

How to Choose the Best Loan Origination System

When selecting an LOS platform, financial institutions should evaluate:

CredAble’s AI-Enabled Loan Origination Platform

CredAble offers an AI-powered Low-Code Loan Origination System designed for banks and NBFCs.

Key Capabilities

- Low-code workflow builder for faster product launches

- Integration with India’s digital data infrastructure

- AI-driven underwriting and decision support

- Policy-based decisioning with full traceability

- Unified platform across lending products

This enables institutions to scale lending while maintaining speed, control, and compliance.

People Also Ask -

A loan origination system is a digital platform that helps banks manage the complete loan journey from application intake and borrower verification to credit underwriting, approval, documentation, and disbursement. It brings lending teams, data sources, workflows, and compliance checks into one structured system.

Banks need a loan origination system to reduce manual work, improve loan approval speed, maintain consistent credit decisions, and scale lending operations. A modern LOS helps banks process higher loan volumes while keeping risk, compliance, and audit controls in place.

A loan origination system improves loan approval speed by automating data collection, document verification, credit bureau checks, underwriting workflows, approval routing, and borrower communication. This reduces delays caused by manual data entry, fragmented systems, and repetitive checks.

Key features of loan origination software include digital application intake, KYC and document management, credit bureau integration, automated underwriting, workflow configuration, compliance checks, approval management, eSign support, and core banking system integration.

An AI powered loan origination system helps banks analyse borrower data faster, identify risk patterns, generate credit insights, support underwriting decisions, and improve consistency across applications. It can also help banks evaluate cash flows, financial behaviour, and alternative data signals more effectively.

A loan origination system manages the loan process before disbursement. This includes application, underwriting, approval, and documentation. A loan management system manages the loan after disbursement, including repayment schedules, collections, servicing, and account management.

Yes. A modern loan origination system can support SME and business lending by enabling cash flow based assessment, document automation, GST and banking data integration, invoice based lending workflows, working capital financing, and customised credit approval rules.

Banks should choose a loan origination system based on integration capability, workflow flexibility, AI and data analytics, compliance readiness, deployment model, scalability, user experience, and the ability to support multiple lending products across digital and assisted channels.

Yes. A cloud based loan origination system can help banks and NBFCs deploy faster, scale more efficiently, reduce infrastructure dependency, and support continuous upgrades. It is especially useful for institutions looking to launch new lending products quickly.

CredAble’s AI enabled low code loan origination system helps banks and NBFCs build, launch, and scale lending journeys with configurable workflows, digital data integrations, AI driven underwriting support, policy based decisioning, and full traceability across the loan lifecycle.

Think Working Capital… Think CredAble!